What is a Retirement Compensation Arrangement (RCA)?

A Retirement Compensation Arrangement (RCA) is ideal for high-income earners ($150,000+) such as business owners, incorporated professionals, executives and athletes who wish to sustain their standard of living into retirement, an RCA represents the highest level of retirement program available in Canada. An RCA allows a company to make tax-deductible contributions on behalf of key employees for purposes of retirement to the maximum level allowable. The flexibility of the RCA allows it to be adapted to many business and tax strategies. The RCA requires a sponsoring company in order to set it up.

An RCA is Often Used in the Following Situations:

- Intergenerational benefit and the family business

- Expatriate executives and athletes.

- Golden handcuffs; key executives’ retention

- Sale of a business

Key Benefits of an RCA:

- Flexible

- Funds are not locked in

- Creditor-proof

- Exempt from payroll taxes

- Ability to reduce amount of taxes paid by lowering participant’s tax rate

- Taxation only occurs at the time of withdrawal

- Taxation depends on place of residency at time of withdrawal

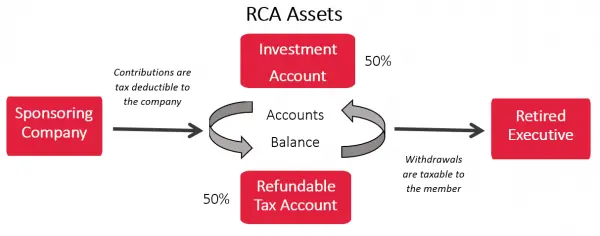

Allocation of Contributions:

Each year the company may choose to make contributions on behalf of the members of the plan, who may also be required to contribute to the RCA. 50% of these contributions are made to an RCA Trust investment account. The other 50% is remitted to a refundable tax account (RTA) with Canada Revenue Agency (CRA). Half of any net realized investment income is remitted to the RTA on an annual basis also. Similarly, the investment account can recover half of net losses to the extent refundable tax has been remitted on realized gains in prior years.

Investment Account:

The investment account is managed by plan trustees and directed by the company or the principal plan member. There are few investment rules or restrictions, however, it is recommended that the investments be of a non-distributing nature, as 50% of all dividends, realized capital gains and interest income less expenses must be remitted annually to the RTA.

Withdrawals:

Upon retirement or a change of employment status the beneficiary will draw from the assets of the RCA Trust. An amount equal to 50% of the distribution from the investment account will be refunded to the RCA from the RTA account after a Tax Return has been completed at the calendar year-end. Withdrawals are flexible and not subject to any restrictions on maximum or minimums. They are however, subject to withholding tax at a rate of 30% if located in Canada.

No Required Retirement Date:

Provided there is a change of employment status the member of the RCA may begin withdrawals from their RCA at any age they wish. By the same token, there is no requirement to begin withdrawals at age 71, like RRSPs. The assets of the RCA may remain in the Trust Fund throughout the lifetime of the member and may subsequently be used for the benefit of spouses and beneficiaries.

Final Things You Need to Know:

- Watch for Salary Deferral Arrangement (SDA) when structuring member’s benefits.

- As long as the contributions are reasonable, large tax-deductible contributions may be put into an RCA resulting in substantial tax relief to the company.

- To ensure reasonableness, GBL certifies every RCA with an actuarial certificate. This calculation is based upon the member’s best three years’ T4 earnings and period of service.

Talk to Statera Financial Planners today & see if an RCA is the right strategy for your business!